What does the updated Community Reinvestment Act mean for digital equity?

Three features of the final CRA rule that can help unlock funding for broadband

In October, federal banking regulators issued updated Community Reinvestment Act (CRA) rules that will shape the future of community development finance.

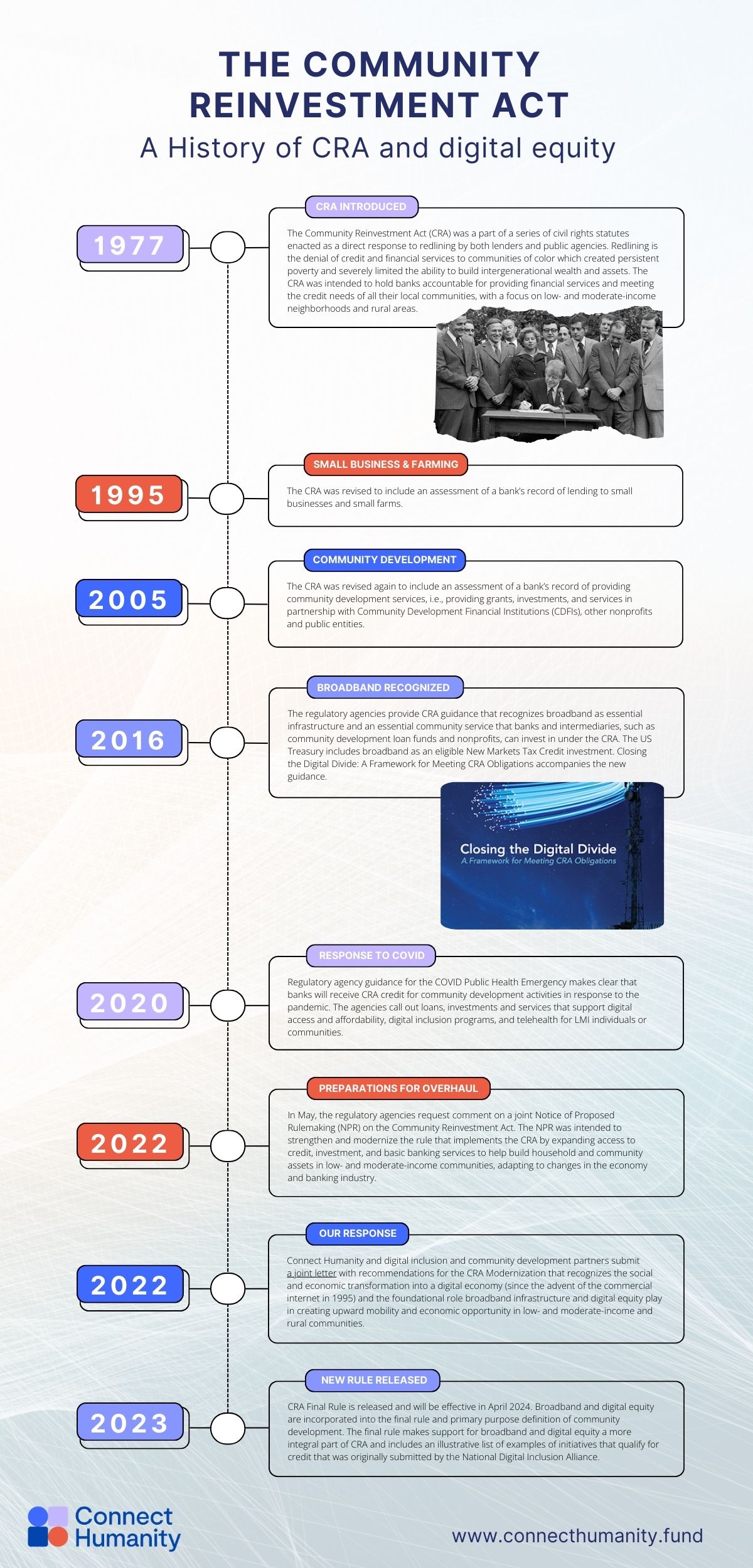

Passed in 1977, the CRA requires banks and savings associations to meet the credit needs of the communities they serve, with the aim to reverse the harmful legacy of redlining and disinvestment, particularly in communities of color. Last overhauled almost 30 years ago at the dawn of the world wide web, CRA rules were overdue an update to make them responsive to the needs of low- and moderate-income, rural, and underserved communities in the expanding digital economy.

So, when a proposal to modernize the regulations was issued last year, those of us working to close the digital divide mobilized to ensure the rules reflect the importance of broadband as essential infrastructure for accessing financial services and promoting opportunities for upward mobility. In coordination with digital inclusion and community development leaders across the country, Connect Humanity provided recommendations to this Notice of Proposed Rulemaking for CRA Modernization.

How does the new CRA address the digital divide?

We’re pleased the CRA Modernization Final Rule issued in October 2023 reflects the spirit of the recommendations we made, and gives greater priority to digital equity. Here are some highlights:

1. The Final Rule includes broadband in the primary purpose definition for community development investments

Bank Lending, Service, and Investment qualify under CRA when the “primary purpose” of the activity is for community development. The new definition of community development includes eleven categories of activity that fulfill CRA obligations, including: Affordable housing; Economic development; Community supportive services; Essential community infrastructure; and more (see p119-120 for the full list).

The new rule updates the definition to directly include broadband under four of the eleven categories, including: Community Supportive Services [§ __.13(d)], Community revitalization or stabilization [§ __.13(e)], essential community facilities [§ __.13(f)], and essential community infrastructure. [§ __.13(g)].

Delivering on our recommendation for a clear statement that broadband and digital inclusion meet the “primary purpose” definition of CRA, this is a significant step forward from the last guidance in 2016 which listed broadband as an example in just one category (essential community infrastructure). By including broadband so prominently in the primary purpose definition, the new rule sends a strong signal to banks of the importance of digital equity in community development and CRA.

2. Greater priority for community development finance and grants available for broadband

Under the CRA, Large Banks are evaluated based on four tests. The new rule weights these as: Retail Lending (40 percent), Retail Services and Products (10 percent), Community Development Financing (40 percent), and Community Development Services (10 percent).

The weighting for the Community Development Finance Test, from which significant broadband investments will flow, has been increased to 40 percent from the initially proposed 30 percent, growing the size of the pie for broadband investments.

While the Retail Lending Test remains important for direct bank financing of broadband infrastructure, this increase in community development investments will mean more funds available to community loan fund intermediaries to invest in broadband projects.

3. Recognizes the changing nature of banking by incentivizing banks to invest in connectivity and digital skills to support access

The CRA includes a service test that measures whether banks make their services easily available and accessible to people living on low- and moderate incomes. Traditionally this test has been based on having physical branches in and around underserved communities.

Now, access to mobile and online banking is factored in, with the Retail Services and Products Test examining the effectiveness of large banks’ digital services to meet the service needs of LMI communities.

This change incentivizes banks to invest in connectivity and skills programs to help their customers access digital services. Banks now have opportunities to layer funding for digital equity programs alongside connectivity investments, reinforcing the value of each. For example, a large bank investing in a non-profit loan fund to expand internet access in a LMI neighborhood could make a complementary grant to fund a device access program and digital navigators to support residents with the technology and skills they need to use the bank’s app and online services. Together, these activities would 1) qualify as a community development investment 2) count towards the retail service test and 3) count towards the community development services test through skills training.

Layering investments and grants in this way is a powerful way to deepen the impact of CRA funds and demonstrate innovation, which is highly valued in CRA evaluation.

Another significant change that will open up more funds from large banks for broadband infrastructure and digital equity is the move away from requiring banks to only focus on areas where they have physical branches. As our joint letter recommended, the new rule gives credit for lending, service and investment in any US persistent poverty location or region, recognizing that banks are less geographically bounded in the age of digital of banking.

Implementation of the Final Rule

The Final Rule becomes effective April 1, 2024. However, most of the new CRA rules apply starting on January 1, 2026, with the remaining rules, including reporting requirements, in place from January 1, 2027. But banks and CDFIs should not wait to increase lending and investing for broadband and digital equity. Digitalization clearly fits within the scope of the Community Reinvestment Act and intersects all areas of community development. The need for investment in this area is urgent — with hundreds of viable, sustainable community-focused broadband projects across the country, spurred by the Infrastructure Investment and Jobs Act, poised to help close the digital divide, given the right community development partners.

Agencies have committed to increasing transparency and conducting outreach and training for banks to understand the opportunities and obligations under the new rule. Connect Humanity and our partner organizations look forward to working with the agencies to help develop training and case studies on CRA broadband investment and digital equity.

Connect Humanity has created new community development finance instruments for broadband and digital equity. To talk with us about leveraging CRA investments to invest in digital equity projects, email us at info@connecthumanity.fund.

A history of the CRA and Digital Equity

Keep in touch

To learn more about our work follow us on social media, subscribe to our newsletter, and write to us anytime at info@connecthumanity.fund.